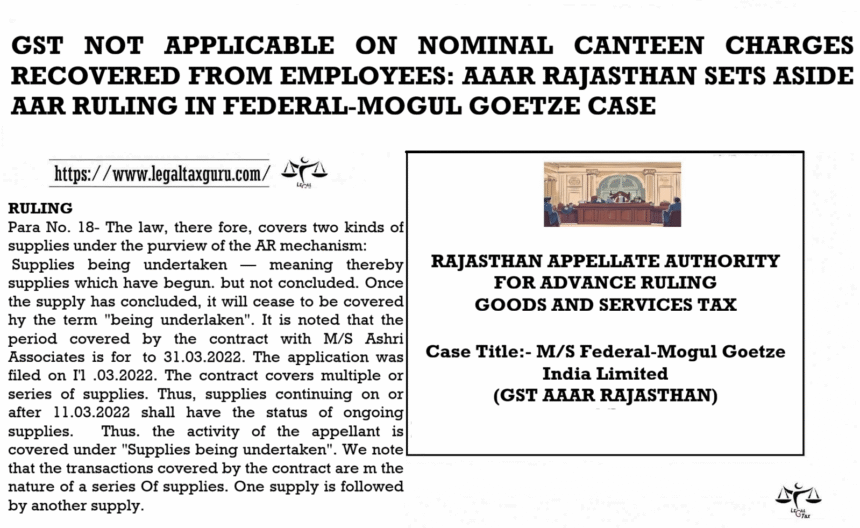

GST NOT APPLICABLE ON NOMINAL CANTEEN CHARGES RECOVERED FROM EMPLOYEES: AAAR RAJASTHAN SETS ASIDE AAR RULING IN FEDERAL-MOGUL GOETZE CASE

RAJASTHAN APPELLATE AUTHORITY FOR ADVANCE RULING

GOODS AND SERVICES TAX

Before the Bench of

1. Sh. Mahendra kanga. Member (Central Tax)

2. Dr. Ravi Kumar Surpur, Member (State Tax)

Case Title:- M/S Federal-Mogul Goetze India Limited (GST AAAR RAJASTHAN)

Appeal No. RAJ/AAAWAPP/06,’2022-23

Advance Ruling No. RAJ/AAR’2022-23/13 dated 18.10.2022

Date of Judgement Order-15th March 2024

BRIEF OF FACT

Para No. 2- The Appellant had sought Advance Ruling on the following questions: — Whether the subsidized deduction made by the Appellant from the Employees who are availing food facility in the factory would be considered as a “supply” by the Appellant under the provisions of Section 7 of Central Goods and Service Tax Act, 2017 and Rajasthan Goods and Service Tax Act, 2017.

- In case answer to above is yes,

l. Whether GST is applicable on the nominal amount deducted from the salaries of their employees?

Il. Whether GST would be applicable on the nominal amount deducted from the Manpower supply contractor in case of contractual employees?

- Whether Input Tax Credit (‘ITC’) of the GST charged by the Canteen Service Provider would be eligible for availment to the Appellant?

Para No. 3- The Appellant have contracted with m/s Ashri Associates (hereinafter referred to as ‘the Canteen Service Provider’) to operate Canteen within the Appellant’s factory premises; and a part Of the cost Of the meals provided is deducted by the Appellant from their employees’ salaries on a monthly basis and at fix rate opting for availing food facility in Canteen. A part of the cost of the meals provided to contractual workers is recovered from contractor in case of contract workers. The Appellant are paying GST against supply of canteen service on recovery basis since July 2017.

GROUDS OF APPEALS

Para No. 6- The Appe114nt have filed an appeal on the following grounds:

6.1 Illat the definition meaning of the term ‘ongoing’ is ‘continuing’, ‘still in progress’. In the instant .case. the transaction although is being undertaken since July, 2017, it is still being undertaken and will be undertaken in the future also.

6.2 Appellant submitted that going by the meaning of the term ‘ongoing’ it can be said that the transaction being undertaken by the appellant falls within the purview of definition Of ‘Advance Ruling’ prescribed under Section 95 of the CGST Act.

6.3 The Appellant further submitted that the Central Board of Indirect Taxes and Customs (hereinafter referred to as ‘the CHIC’) in nyer on Advance Rulings has clarified that under GST. Advance Ruling can be obtained ror a proposed transaction as well as transaction already undertaken by the Appellant. The relevant extract of Ole flier is reproduced below: under the present dispensation. advance ruling can be given only for a proposed tramcaction. whereas under GEST advance ruling can he obtained for a proposed transaction as well as mmsaction already undertaken by the applicant ‘

6.4 The Appellant placed reliance on Advance Ruling pronounced by the Appellate Authority for Advance Ruling, Rajasthan in the matter of m/s Shri Vinayak Build con 12022(5) TMI 450, Rajasthan

6.5 Reliance in this regard is also placed on the Ruling pronounced in the matter Of M/s KEI Industries Limited 12019 (3) TMI 1073, Rajasthan]

6.6 Appellant submitted that in the instant case that they wish to seek clarification on (i) admissibility of input tax credit of tax paid or deemed to have been paid and (ii) determination of the liability to pay tax on goods or services or both; of Section 97 of the CGST Act. Thus, both the questions on which Advance Ruling is sought are questions on which an Advance Ruling can be filed. Thus, the Appellant has rightly filed the advance ruling.

RULING

Para No. 18- The law, there fore, covers two kinds of supplies under the purview of the AR mechanism:

- Supplies being undertaken — meaning thereby supplies which have begun. but not concluded. Once the supply has concluded, it will cease to be covered hy the term “being underlaken”. It is noted that the period covered by the contract with M/S Ashri Associates is for to 31.03.2022. The application was filed on I’l .03.2022. The contract covers multiple or series of supplies. Thus, supplies continuing on or after 11.03.2022 shall have the status of ongoing supplies. Thus. the activity of the appellant is covered under “Supplies being undertaken”. We note that the transactions covered by the contract are m the nature of a series Of supplies. One supply is followed by another supply.

- Proposed to be undertaken – There is no doubt about supplies which are yet to cornmcnce us these are without any doubt covered by the AR mechanism.

Therefore. we hold that the Authority for Advance Ruling. Rajasthan has erred in not pronouncing the Ruling on Merits.

Para No.19 – We observe that AAR Rajasthan have not taken note Of the above contract fumished by the appellant for the period from 01.04.2021 to 31.03.2022. which was valid during the period when Ruling was pronounced.

Para No.20 – We feel that it will be in the fitness of things if the Authority for Advance Ruling re-consider whole application dated 1 1.03.2022 filed by the appellant before the Authority for Advance Ruling, Rajasthan on merits.

ORDER

Para No. 21- In view of the above discussions. we pass the following order:

The Ruling of AAR, Rajasthan dated 18.10.2022 is set aside and the matter is remanded to the AAR to decide the application afresh on merits after considering all the submissions made by the appellant in their application dated 18.10.2022.