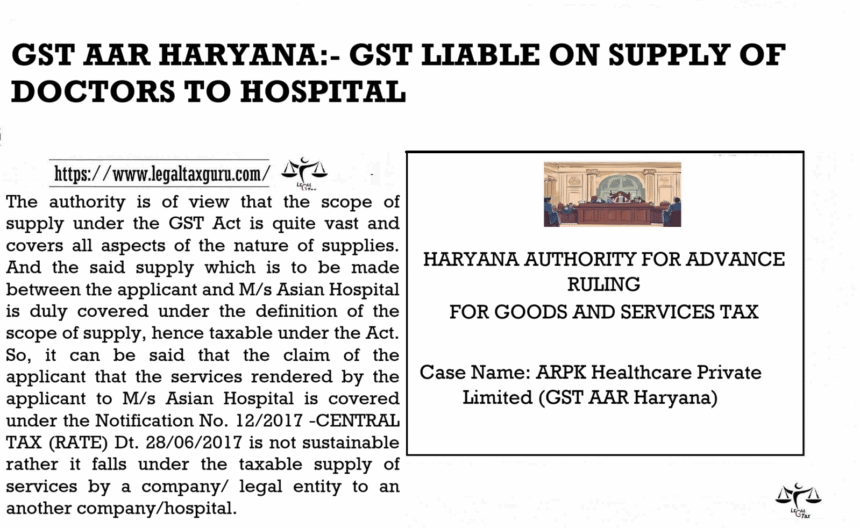

GST AAR HARYANA:- GST LIABLE ON SUPPLY OF DOCTORS TO HOSPITAL

HARYANA AUTHORITY FOR ADVANCE RULING

FOR GOODS AND SERVICES TAX

Case Name: ARPK Healthcare Private Limited (GST AAR Haryana)

Appeal Number: Advance Ruling No. HR/HAAR/07/2022-23

Date of Judgement/Order: 12th January 2023

CONCLUSION

The authority is of view that the scope of supply under the GST Act is quite vast and covers all aspects of the nature of supplies. And the said supply which is to be made between the applicant and M/s Asian Hospital is duly covered under the definition of the scope of supply, hence taxable under the Act. So, it can be said that the claim of the applicant that the services rendered by the applicant to M/s Asian Hospital is covered under the Notification No. 12/2017 -CENTRAL TAX (RATE) Dt. 28/06/2017 is not sustainable rather it falls under the taxable supply of services by a company/ legal entity to an another company/hospital.

RULING

Questions 1. Whether Fee/ charges received by M/s ARPK from M/s Asian is exempt under GST?

Answers: – No

Questions No 2. Whether Fee/charges for Health Care Services received by M/s Asian is exempt under GST.

Answers: – Yes except for the services mentioned under heading 9993 clause no. 31A vide Notification 03/2022-Central Tax(Rate) dated 13.07.2022.